Release Notes

Last updated: 2026-06-24

Feedback

Do not hesitate to provide us with feedback using the contact form (or from the support section on your MantaTrade account).

Roadmap

- Q3 2026 - MantaWealth - Instrument screener

- Q3 2026 - MantaWealth - Portfolio book monitoring

- Q4 2026 - MantaWealth - UI for mass rebalancing (currently only available on the API)

- MantaWealth - Suggested instruments for diversification

- MantaAPI - Additional coverage for derivatives

- MantaAPI - Additional coverage for structured products

- MantaAPI - AI based country exposure

- MantaWealth - Expected returns according to Black-Litterman

- MantaWealth - Non-Linear Optimisation engine for preference driven investment

- MantaTrade - eToro integration

- MantaTrade - Portfolio monitoring: Unusual Price Action

- MantaTrade - ability to save and monitor setups

2026-06-24 Release 6.0

MantaWealth / MantaAPI - Methodology update: VaR & CVaR

- VaR and CVaR are now computed on demeaned returns — the historical mean is subtracted before estimating the loss quantile — so tail risk is measured independently of expected return (Rockafellar–Uryasev–Zabarankin, 2006).

- Portfolios with a positive historical drift will therefore show higher CVaR/VaR; those with a negative drift, lower.

- CVaR and VaR (incl. contributions) are no longer published above a monthly horizon (quarter, YTD, year), where time-scaling is unreliable under fat tails — long-horizon and crisis tail risk is covered by our stress-testing / scenario analysis instead.

2026-05-17 Release 5.5

- MantaWealth - Private Asset Management: private assets are now managed directly from the MantaWealth front-end, bringing the proxy-based coverage previously available on MantaAPI into the UI.

- MantaWealth / MantaAPI - Report Configuration: organisation-level defaults for PDF Investment Proposals (co-branding, report sections) can now be saved and reused, and overridden per-report when needed.

2026-04-27 Release 5.4

- MantaWealth - Investment Proposals: a new PDF Report button generates a professionally formatted, client-ready portfolio analysis in a single click — covering allocation, risk metrics, and rebalancing recommendations. Ideal for client meetings, advisory reviews, and compliance documentation.

See a sample output here: Investment Proposal (example PDF).

2026-04-18 Release 5.3

- Release of the MantaRisk MCP Server: AI assistants can now connect directly to MantaRisk to create portfolios, run analytics, and trigger rebalancing.

2026-03-14 Release 5.1

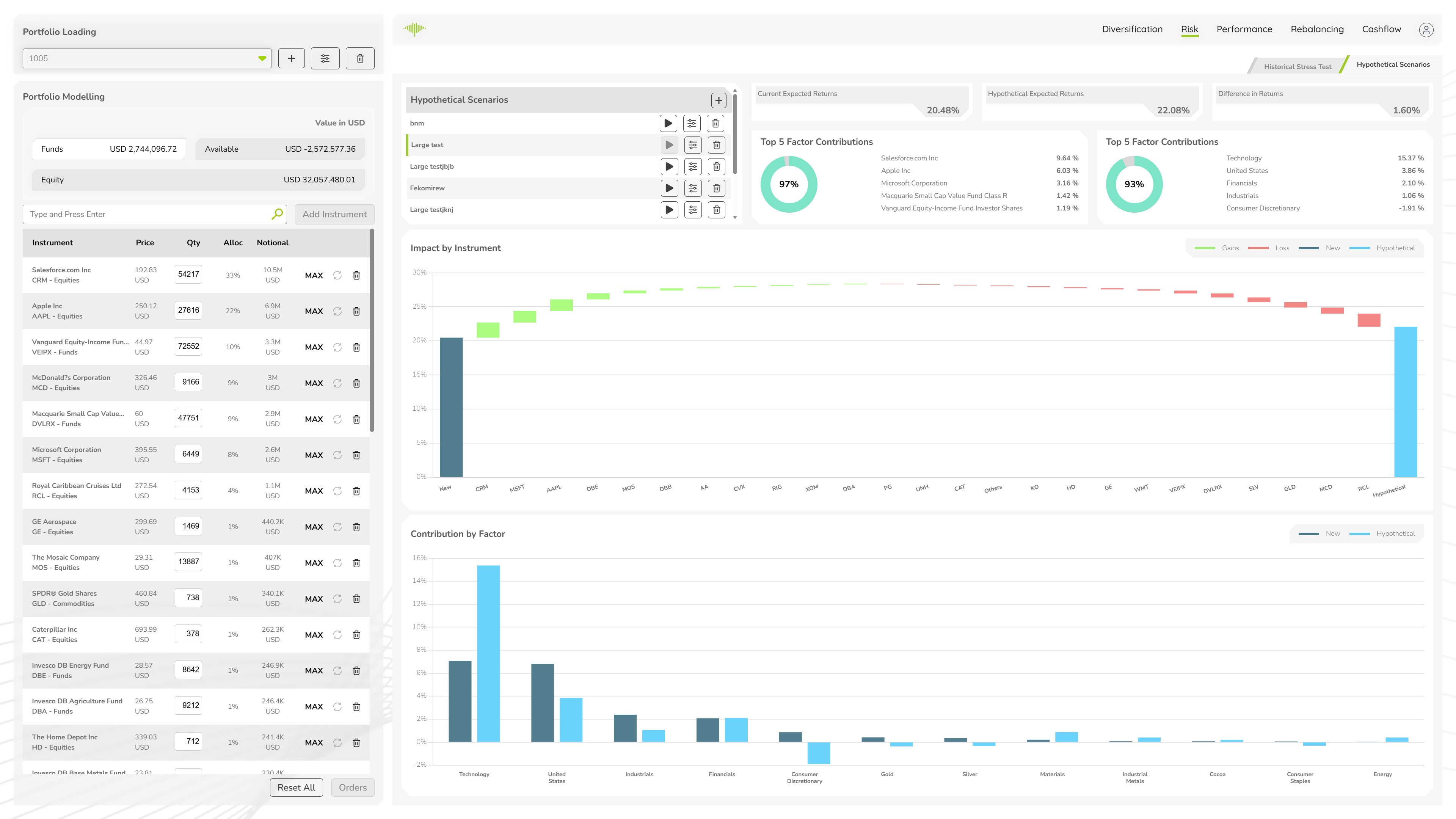

- MantaWealth - Factor based hypothetical stress testing

2026-03-10 Release 5.0

- MantaWealth / MantaAPI - backend performance improvements

- MantaAPI - Factor based hypothetical stress testing

2026-02-21 Release 4.2

- MantaAPI - Coverage for private assets (proxy)

- MantaWealth - UI performance enhancements

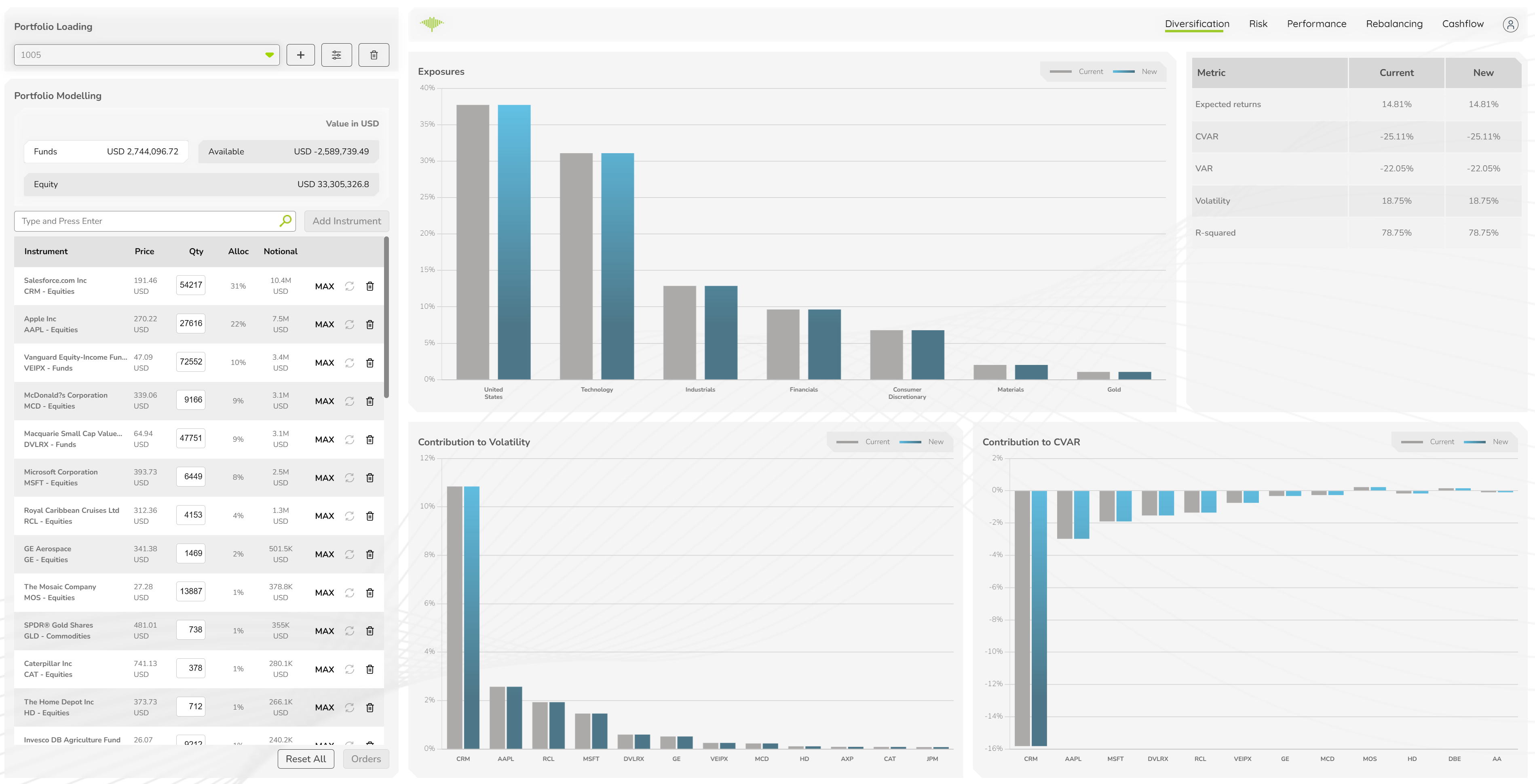

- MantaWealth - upgraded diversification screen

- MantaAPI - support for CUSIPs

- MantaAPI - new endpoint to calculate a portfolio's PnL

- MantaAPI - ability to automatically adjust for dividends and splits on portfolio upload

2025-12-14 Release 4.0

- MantaAPI / MantaWealth - Cashflow forecasting

- MantaAPI - Composite benchmarks made of 2 or more sub-benchmarks

- User configurable asset classifications

- Portfolio Analytics: VaR, CVaR, and expected return aggregated by asset class and sector

- Portfolio Analytics: contribution to portfolio VaR and CVaR broken down by asset class, sector, and individual securities

- Updated billing endpoint with client breakdown for distributors

- Performance Improvements

2025-09-04 Release 3.6

- UI Integration with WealthArc

2025-08-26 Release 3.5

- New /portfolio/benchmark endpoint to correlate an entire portfolio to a specific price curve (alpha, beta, idiosyncratic risk, CVAR). Allows for calculations of exposures to custom factors.

- Faster instrument search functionality

2025-07-26 Release 3.4

Integration with Portfolio Management System Addepar. Our clients can now use their Addepar API keys to have direct access to their portfolios from MantaWealth.

2025-06-16 Release 3.2.6

Update of /analytics endpoint: introduction of additional calculations for expected return:

- Sample based expected returns

- Factor based expected returns

Both are available either equally or exponentially weighted and over daily, weekly and monthly timeframes.

2025-06-03 Release 3.2

- MantaAPI - Backtesting performance improvements

- MantaAPI - Additional equities data coverage

- MantaAPI - New "Data coverage checker" endpoint allowing rapid translation of ISIN / Currency pairs into our instruments.

- MantaAPI - Introduction of Hierarchical Multi Asset Class attribution as an alternative to Brinson Fachler for multi asset portfolios.

2025-03-04 Release 3.1

- MantaWealth - Performance Attribution Analysis UI

- MantaAPI - Performance improvements for loading portfolios

2025-02-23 Release 3.0

- MantaAPI - Short positions

- MantaAPI - Leveraged instruments

- MantaAPI - Coverage and model for Fixed Income

2025-01-30 Release 2.0

- MantaAPI - Performance Attribution Analysis now available. See the API Reference for more details.

2025-01-26 Release 1.4

- All - New account management system: subscriptions can now be directly purchased online through Stripe integration.

- All - Improved historical PnL calculation: PnL is now calculated against historical capital available as opposed to max capital required.

- MantaWealth - Minor UI improvements, security improvements (introduction of single use tokens)

2024-11-22 Release 1.3

- All - Private instances: ability to run our engine privately i.e. within your own architecture

- MantaWealth - Performance improvements

2024-10-14 Release 1.2

- Introduction of pure Maximum Diversification algorithm (Choueifaty and Coignard)

- MantaWealth - Instrument search UI fixes

2024-10-05 Release 1.1

- Introduction of Benchmark Tracking algorithm

- New MantaRisk Website

- Multiple bug-fixes

2024-09-08 Release 1.0

- Release of MantaWealth - our Portfolio Construction Application

- Constraints Based Optimisation: ability to constaint portfolio construction based on geographies, sectors, currencies and individual instruments

- Integration with WealthArc

2024-06-30 Release Candidate 0.5

- Improvements to API health monitor: 2 mins heartbeat, additional tests

- Extensive functional testing pass 2 out of 3 completed

- Backtesting FX conversions issue fixed

- Stale historical data issue fixed

- Improvement in exposure determination

- Alpha caculation now follows Capital Asset Pricing Model

- Performance improvements:

- Historical data for daily timeframe pre loaded

- Exposure pre calculated

- Portfolio Management Application MVP available

2024-06-02 Release Candidate 0.1

- Introduction of API health monitor to ensure fast response from support team

- Extensive functional testing pass 1 out of 3 completed

2024-04-24 Beta 3.2

Publication of new endpoint for portfolio level analytics including:

- Correlation based exposure to sectors, countries and currencies

- CVAR over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

- VAR over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

- Volatility over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

- Diversification ratio: metric used to quantify the level of diversification within a portfolio. MantaRisk uses the definition according to Choueifaty and Coignard (2008) where this ratio considers both the number of assets in the portfolio and the correlations between them. A higher diversification ratio indicates a more diversified portfolio, meaning the assets are less likely to move in the same direction, reducing overall portfolio risk.

- Expected return: defined as the average return over 5 years on a daily, weekly or monthly timeframe

- R Squared: proportion of the variance explained by the risk factors. 1 - R^2 is therefore equivalent to the idiosyncratic risk i.e. the portion of the portfolio which cannot be explained by the risk factors.

2024-04-06 Beta 3.1

- Benchmark endpoint: given two time series (actual and benchmark), provides alpha, beta, idiosyncratic risk etc

2024-03-31 Beta 3.0.1

- Bug fixes (single character instrument search, data source page)

- Increase of the memory pool from 4Gb to 20Gb to allow for large portfolios calculations (500+ instruments)

2024-03-21 Beta 3.0

- Explainable Risk Factors: instrument analytics now provide the exposure of a specific instrument (or price curve) to sectors / countries / currencies

- New API users screen for strategy construction

2024-03-04 Beta 2.0.1

New endpoint to provide instrument (or price curve) level analytics. Given a time serie, provides:

- (Correlation based exposure to sectors, countries and currencies) -> next release

- CVAR over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

- VAR over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

- Volatility over daily, weekly and monthly periods for the 2.5%, 5% and 10% quantiles

2024-03-03 Beta 2.0

- New data source added, now covering 162,435 instruments across stocks, forex, crypto, funds, indices and ETFs. Global coverage including EU market at intraday level

- Performance improvements (co-location of services, local instrument search)

- New Day Trading UI available for Platform users

2024-02-02 Beta 1.9

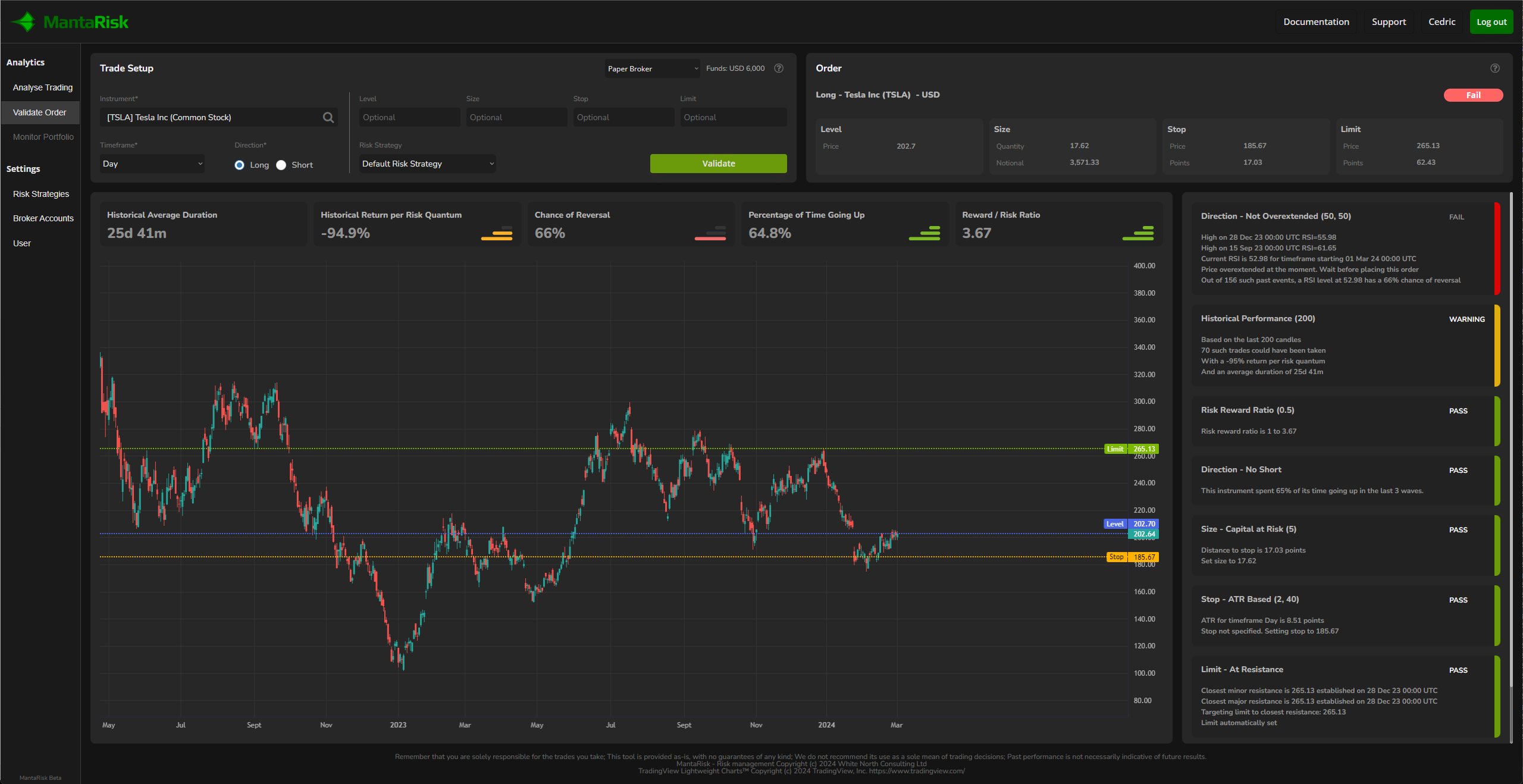

Draft UI to analyse a portfolio management strategy made available to API users.

2024-01-27 Beta 1.8

- Migration of tactical engine to target state infrastructure with high CPU capacity

- Removal of 30 second timeout constraint (504 / H12 error) on all endpoints

2024-01-26 Beta 1.7

- Backtesting performance improvement: migration of the portfolio risk engine to target state infrastructure with high CPU capacity

- Rebalancing methodology tuning - statistical testing of MantaRisk's risk management methodologies has started and has alread led to multiple algorithmic improvements

- Portfolio analysis performance improvement: pre-loading of latest prices

- Various bug fixes

2024-01-07 Beta 1.6

- Release of the Backtesting Engine to allow the testing of risk management strategies for a given portfolio and period of time

- Improvement of Portfolio Analysis (GET /portfolio/analysis) to include advanced rebalancing (reduction of transaction costs caused by high number of trades)

- Introduction of order management within Portfolio Analysis. Open positions can now be added to the portfolio description (PUT /portfolio). These will be taken into account by the portfolio analysis (GET /portfolio/analysis) when suggested orders are sent back.

- Minor performance enhancements

- Various bug fixes

2023-12-17 Beta 1.5

- Release of the ATR portfolio methodology (see Volatility-based Optimization)

- Release of the Risk Parity portfolio methodology (see Volatility-based Optimization)

- Release of the Volatility portfolio methodology (see Volatility-based Optimization)

- Portfolio risk engine performance improvements

- Various bug fixes