Portfolio Rebalancing (Optimisation)

Last updated: 2026-01-29

1 - Creating a Strategy

1.1 - Through MantaWealth

For pure wealth strategies (see Portfolio Rules ), MantaWealth can be used to create the required strategies (e.g. Min CVAR or Tracking Error Minimization). These can then be seen and used within the API.

To access MantaWealth, enter the following address into browser, making sure MYTOKEN is replaced with your API token.

https://wealth.mantarisk.com/wealth-index?token=MYTOKEN

Then navigate to the rebalancing section where you will be able to add and modify rebalancing strategies. Note that the rebalancing section will remain empty until a portfolio has been selected.

1.2 - Through the API

The /strategy endpoints offer a programmatic way of creating and managing optimisation and risk management strategies. The PUT / strategy endpoint uses references for constraints (e.g. rule_id 21 corresponds to Tracking Error Minimisation) and rules which can be found under the /reference endpoints.

1.3 - Through the Strategy Builder

The Strategy Builder is available to users with a MantaRisk account. It allows complex strategies mixing portfolio and tactical algorithms to be created and tested.

If you are logged in, you can access the strategy builder here, else click on Login -> MantaRisk API.

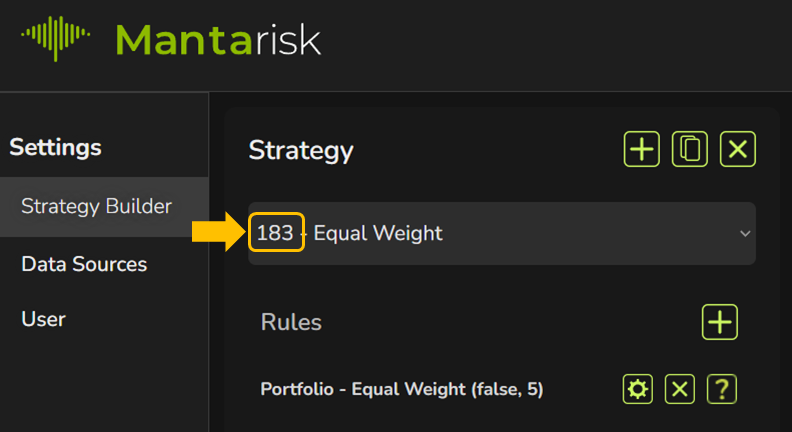

We suggest you use our default strategy to start with. Make note of the number preceeding the name of the strategy. This is the strategy_id and you will need it for later. In the example below 183.

2 - Rebalancing (Optimising) Portfolio(s)

Once a strategy has been created, it can be used to optimise portfolio(s). To do this you must use the /portfolio/rebalance endpoint refering the client_reference and strategy_id from the previous steps.

3 - Backtesting

The /portfolio/backtest endpoints allows the backtesting of a strategy against a specific portfolio. The backtesting is conducted asynchronously as it can take multiple minutes to complete. The GET method can be called to check on the state of the calculations using the status field.